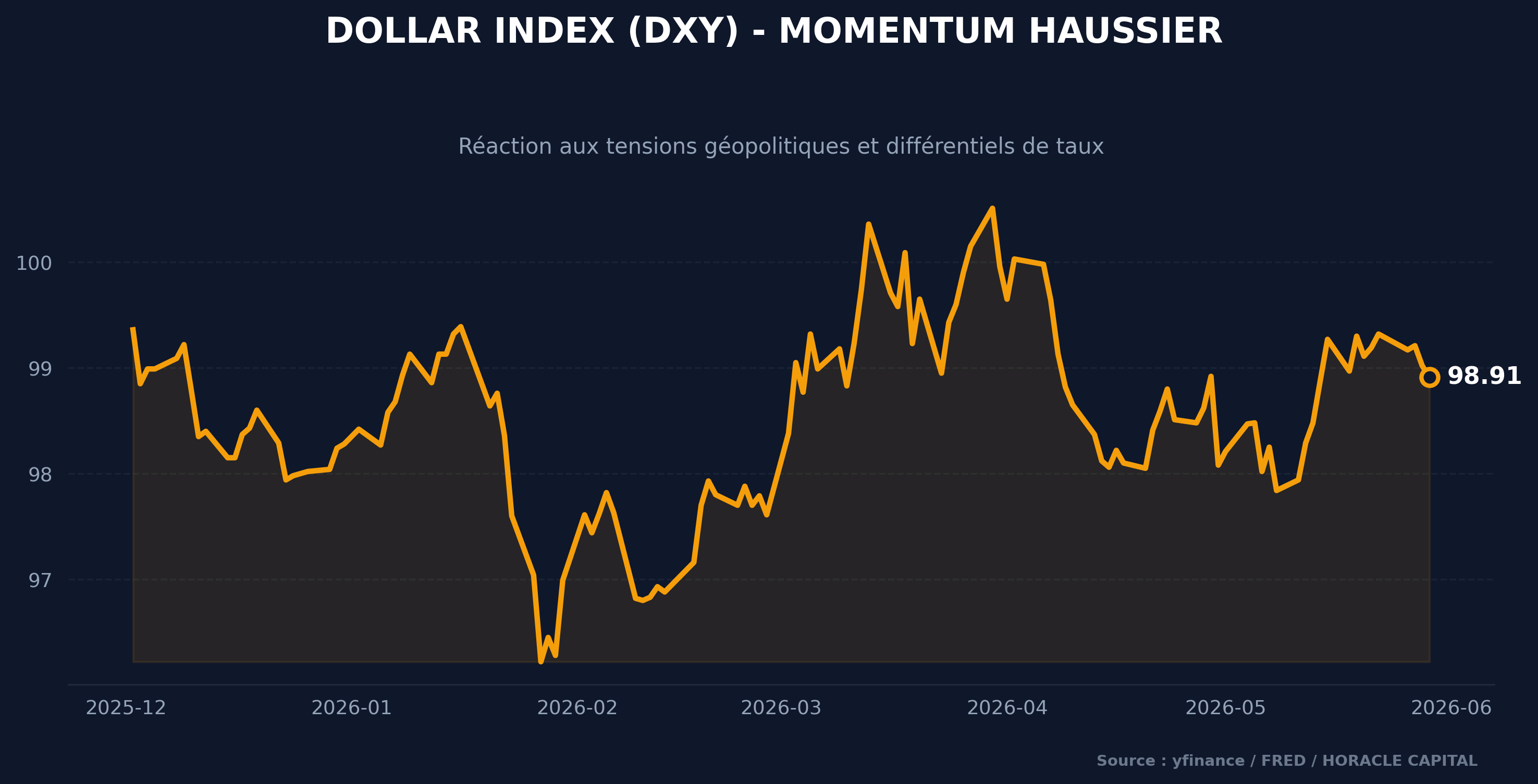

Weekly currency analysis: dollar strengthening, stagflationary pressures in the euro area, and massive interventions on the yen.

USD:

A 60-day extension of the ceasefire had emerged at the start of the week, but military strikes changed the game and pushed the dollar to strengthen. Volatility on the dollar nonetheless remains worth monitoring given the climate in the Middle East.

Capital outflows and the financing needs of foreign central banks weigh indirectly on US government bonds, with the Japanese authorities liquidating part of their US Treasury holdings to fund their FX operations.

Nevertheless, the rational expectations of economic agents push toward a restrictive pricing of the yield curve, which draws international capital flows toward dollar-denominated assets at the expense of risk assets.

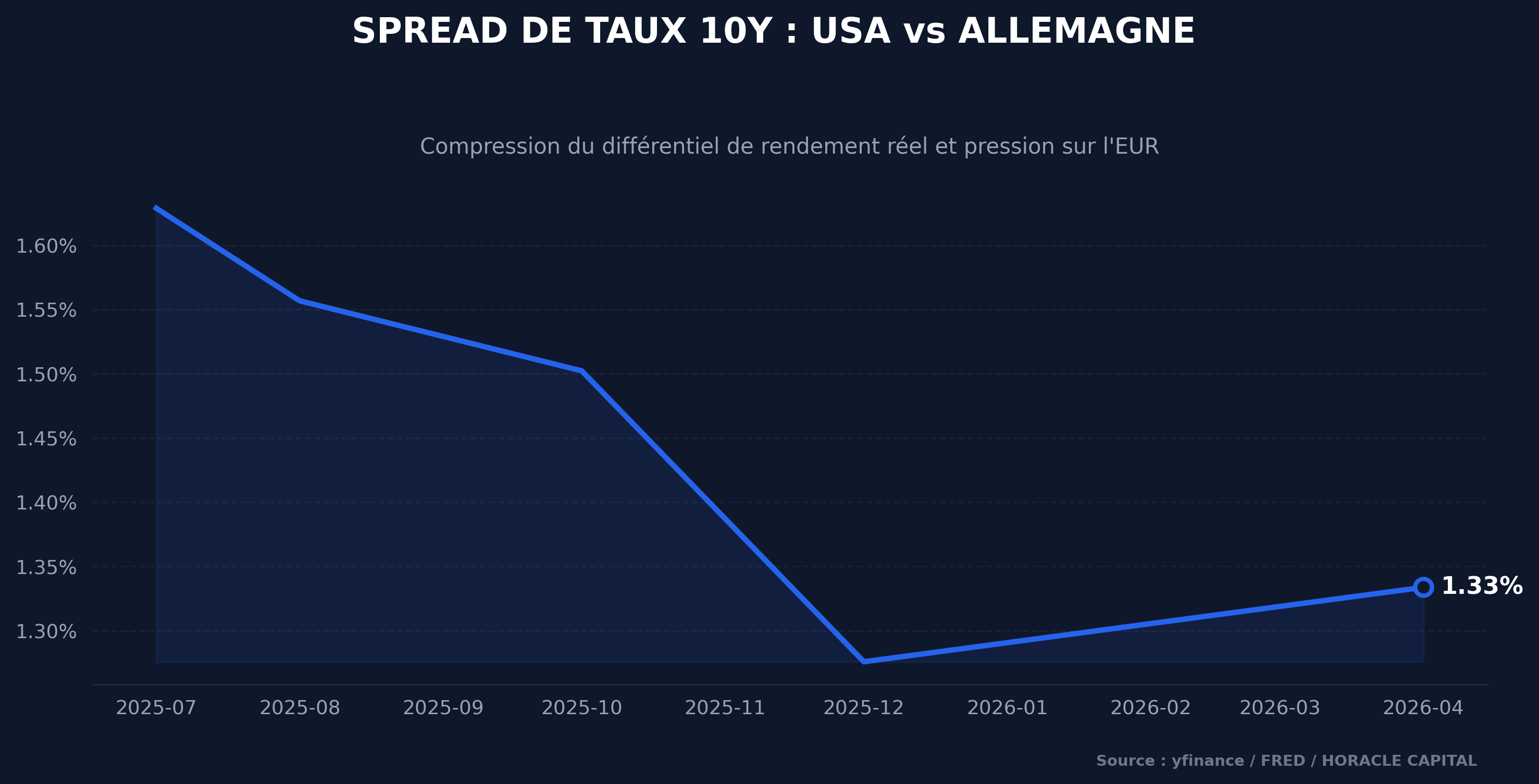

EUR:

The euro area is undergoing an asymmetric stagflationary supply shock. The ECB’s inability to anchor a multi-year restrictive cycle against the Fed compresses the real yield differential. The real interest rate channel no longer plays its role as an automatic stabilizer for the single currency, because the Frankfurt institution is constrained by a growth/inflation trade-off markedly more degraded than that of its US counterpart.

Flash estimates of euro-area inflation reveal an asymmetric dynamic, marked by an acceleration of price pressures in France and Spain while the German indicator shows signs of stabilizing at 2.9%. Although these market projections carry no official status, the emergence of core inflation estimated above the 3.0% mark in Germany is likely to support the short end of the European yield curve by limiting the ECB’s room for maneuver. Through the lens of the rational expectations theory and the Taylor rule, this persistence of cost-push inflation validates the resilience of short-term rates against expectations of aggressive cuts.

The danger: if German inflation were to gain too much momentum, the market could price a larger rate hike, or several 25bps hikes across multiple meetings. Indeed, as highlighted last week, the ECB minutes (the April meeting) showed that the ECB is starting to prepare the ground to accommodate an imminent rate hike, scheduled for the upcoming June 11 meeting, on the basis of a 25bps increase, with 21bps already priced according to ING.

GBP:

As we know, recent weeks in the UK have been marked by political turmoil, with fear and expectations of a more “left-leaning” budget change, hence more constraining for markets. But this week we saw a complete erasure of the 1% political risk premium on EUR/GBP after the conservative budget positioning of front-runner candidate Andy Burnham.

The sharper-than-expected slowdown in inflation invalidates the trajectory of consecutive rate hikes initially priced by markets. By easing the nominal rigidity of prices and wages, the deceleration of CPI reduces the need for the BoE to maintain an overly restrictive hiking curve. The easing of the risk of a budgetary drift to the left neutralizes the risk premium on the pound, stabilizing the EUR/GBP cross below the 0.8700 threshold despite UK unemployment coming in above expectations.

JPY:

Official figures from the Ministry of Finance reveal a massive JPY-buying intervention of 11,735 billion yen (around 74 billion dollars) over the April 28 to May 27 period, marking the largest quarterly currency-stabilization operation since 2004. The JPY is nonetheless undergoing a structural depreciation. The return to a trade-balance surplus validates the activation of the volume effect over the price effect.

However, direct interventions in the FX market prove unable to alter the heavy trend as long as the BoJ maintains deeply negative real interest rates against a restrictive Fed. The financial authorities are moreover structurally limited by the finite stock of their FX reserves and by the need to liquidate US Treasuries to finance the defense of their currency.

The most important point remains, again and again, the risks of inflation and a BoJ rate hike. The market is already starting to price a hike at 78% for the next meeting on June 16. This would endanger carry-trade positions held by large portfolios. Japanese policymakers face a risk of having their exchange-rate regime reclassified from “free floating” to “floating” by the IMF if direct interventions exceed three instances over a rolling six-month period.

On the data front, the unemployment rate remains stable around 2.5% with no notable variation. A slight decline in inflation in the Tokyo region.

CAD:

In parallel, despite the geopolitical volatility of Brent fueled by the strikes in Iran and the halt of logistical transits in the Strait of Hormuz, the Canadian dollar is undergoing a relative depreciation against the greenback. This break from its traditional status as a commodity currency is explained macroeconomically by the deterioration of the Canadian labor market to 6.9% unemployment, the widening of the real interest rate differential against a restrictive Federal Reserve, and the pricing-in of a commercial risk premium linked to the USMCA renegotiations.

NZD:

The Reserve Bank of New Zealand surprised markets at its monetary meeting by keeping its policy rate at 2.25% solely thanks to the casting vote of its governor, Anna Breman, in a tied 3-3 vote. The RBNZ’s new projections signal a clear tightening: the policy rate is now anticipated at 3.00% as early as the start of 2027 (versus end-2028 previously) with a terminal rate revised up to 3.25%. In reaction, the NZD/USD cross appreciated by 0.7%.

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →