Weekly analysis: resilience of US employment, rising inflation in the euro area, the seasonal dynamics of the yen, and the weakness of the Canadian loonie.

Global Context: This week was driven by US employment data. Tensions in the Middle East do not appear to have calmed, with constant strikes coming from both camps. The market seems to have finished pricing in the imminent European and Japanese rate hikes.

Forex

USD

The US labor market appears relatively resilient even though economic activity is not at its peak. Indeed, job openings (April JOLTS) rebound to their highest level since May 2024, the ISM manufacturing index comes in robust, and the ADP survey anticipates a gain of +120k jobs (if you would like to learn more, we have created a series of short videos to explain these concepts).

Friday’s NFP data came out well above expectations, with a consensus of 82k and an actual print of 172k. This pushed the dollar higher and thus sealed the Fed’s fate in terms of rate-hike expectations, with an extremely strong labor market for the month of May.

As we have argued for several weeks, inflationary pressures in the United States do not appear to be slowing. As a result, the rate hike initially priced around 17 bps is now fully integrated by the market, with expectations of 25 bps over the course of this year.

USD-denominated corporate debt issuance shows a volume of 89 bn USD in May, bringing the year-to-date total to 563 bn USD. The banking segment slows to 63 bn USD in May, dominated 63% by senior non-preferred debt. But then, what does this mean for the dollar? International funds are the main issuers of this debt. As a result, in order to subscribe to these highly remunerative securities, foreign institutional investors must sell their local currencies to buy US dollars on the spot FX market, which structurally supports the greenback via the financial account.

The Beige Book paints a picture of economic conditions across the 12 US districts. This report illustrates an overall view of the dynamics and structural challenges facing the United States.

The Fed’s assessment seems to be the consensus one. Inflation in the US zone is gaining ground, and household spending is changing structurally. Indeed, the report illustrates a bifurcation of household spending toward so-called less “discretionary” expenditures. According to the report, US economic activity is advancing at a slow to moderate pace in 10 of the 12 districts.

EUR

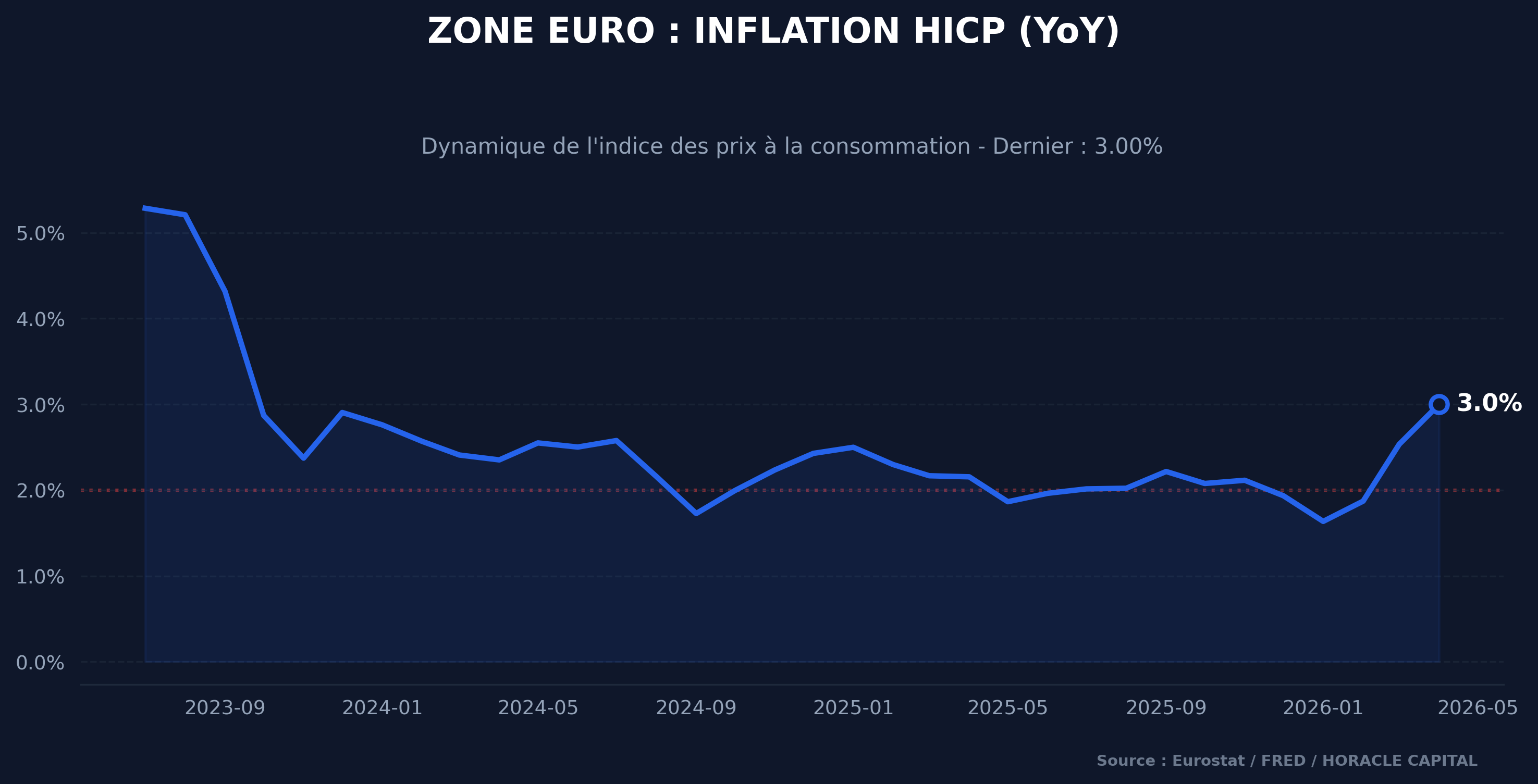

Once again, the euro area is subject to inflation that is gaining ground. Flash headline inflation is expected to rise to 3.2% in May (versus 3.0% previously) and core inflation advances to 2.4%, while the April producer price index jumps to 5% YoY.

Source: FRED / Horacle Capital Analysis

Source: FRED / Horacle Capital Analysis

Moreover, the market fully prices in a 25 bps tightening for the June 11 meeting as well as a second hike in September, even though the 3-year inflation expectations from the household survey decelerated to 2.9% in April. The EUR/USD pair breaks below the psychological 1.1600 level this week to reach 1.1520 late on Friday following the NFP (Non-Farm Payrolls) data releases.

JPY

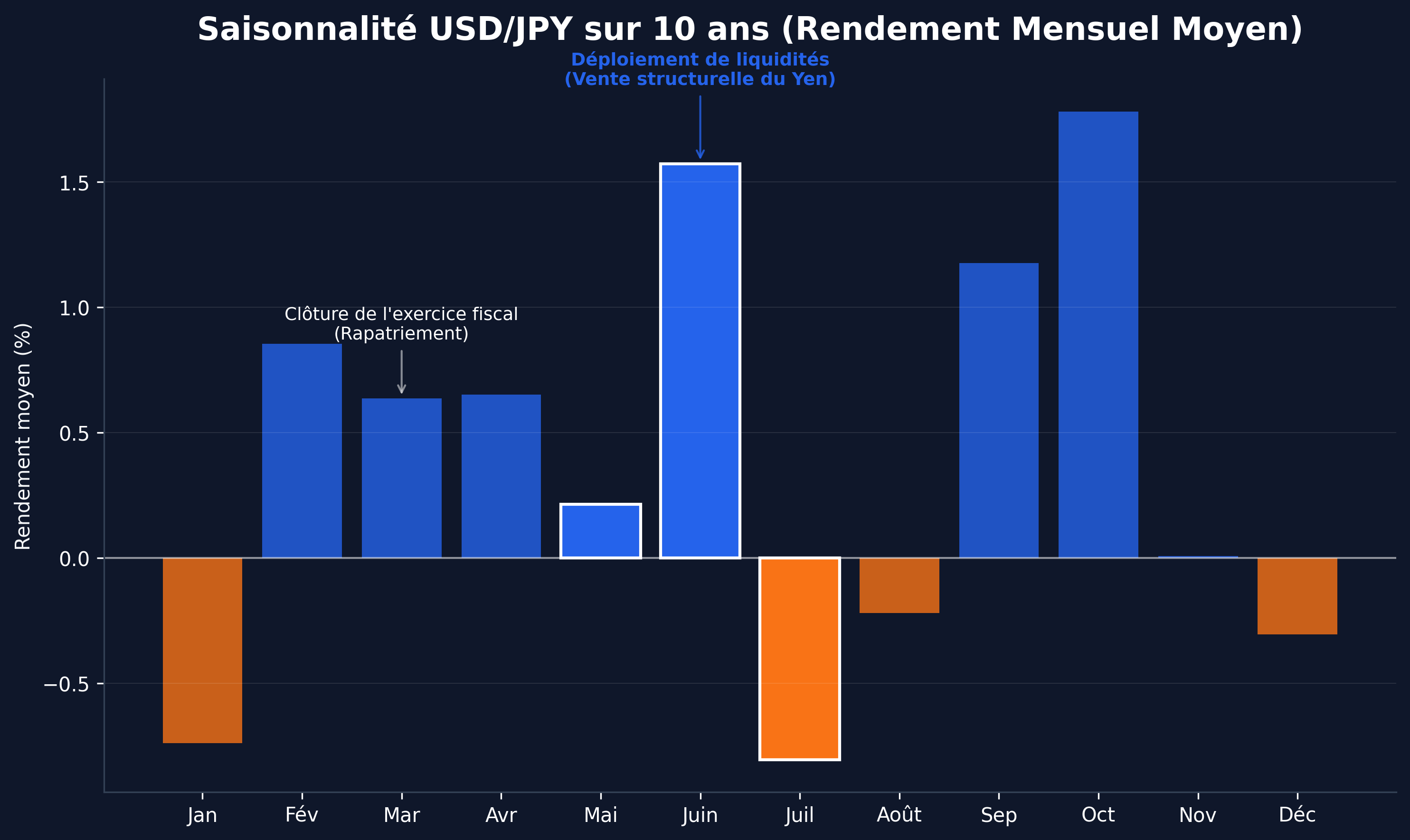

As we already highlighted last week, the actions taken by the Japanese authorities and the BoJ did not have the desired effects on the yen, which continued its depreciation again this week, with the USD/JPY pair reaching the 160 levels.

Source: Yahoo Finance

Source: Yahoo Finance

Structural seasonality: Seasonality prevails over the yen’s depreciation. To understand in more detail, here is a brief explanation: the Japanese fiscal year ends in March, so capital is repatriated to the country. Following this yen-buying movement, around May, June, and July, fresh liquidity is deployed into bond markets and elsewhere, and so selling the yen becomes the new trend for large funds and similar institutions. As a result, the yen’s structural depreciation has a seasonal and accounting character, to keep it simple.

Finally, the COT (Commitment of Traders) suggests a strong selling trend on the yen and buying on the dollar, brilliantly illustrated by the appreciation of the dollar/yen exchange rate.

CAD

The loonie reached its lowest level in 8 weeks following the intensification of tensions in the Middle East.

The Canadian economy validates a phase of contraction in its real output, marked by a decline of -0.1% in annualized terms in the first quarter, confirming the cyclical fragility opened by the -1.0% drop recorded in the previous quarter.

The imposition of 12.5% tariffs by the Trump administration, combined with the escalation of geopolitical tensions in the Middle East, acts as a double external shock directly altering the country’s trade flows and industrial outlook.

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →