Technical and fundamental analysis of the strain on bond yields and its impact on multi-asset portfolios.

The cause: hedging as the watchword

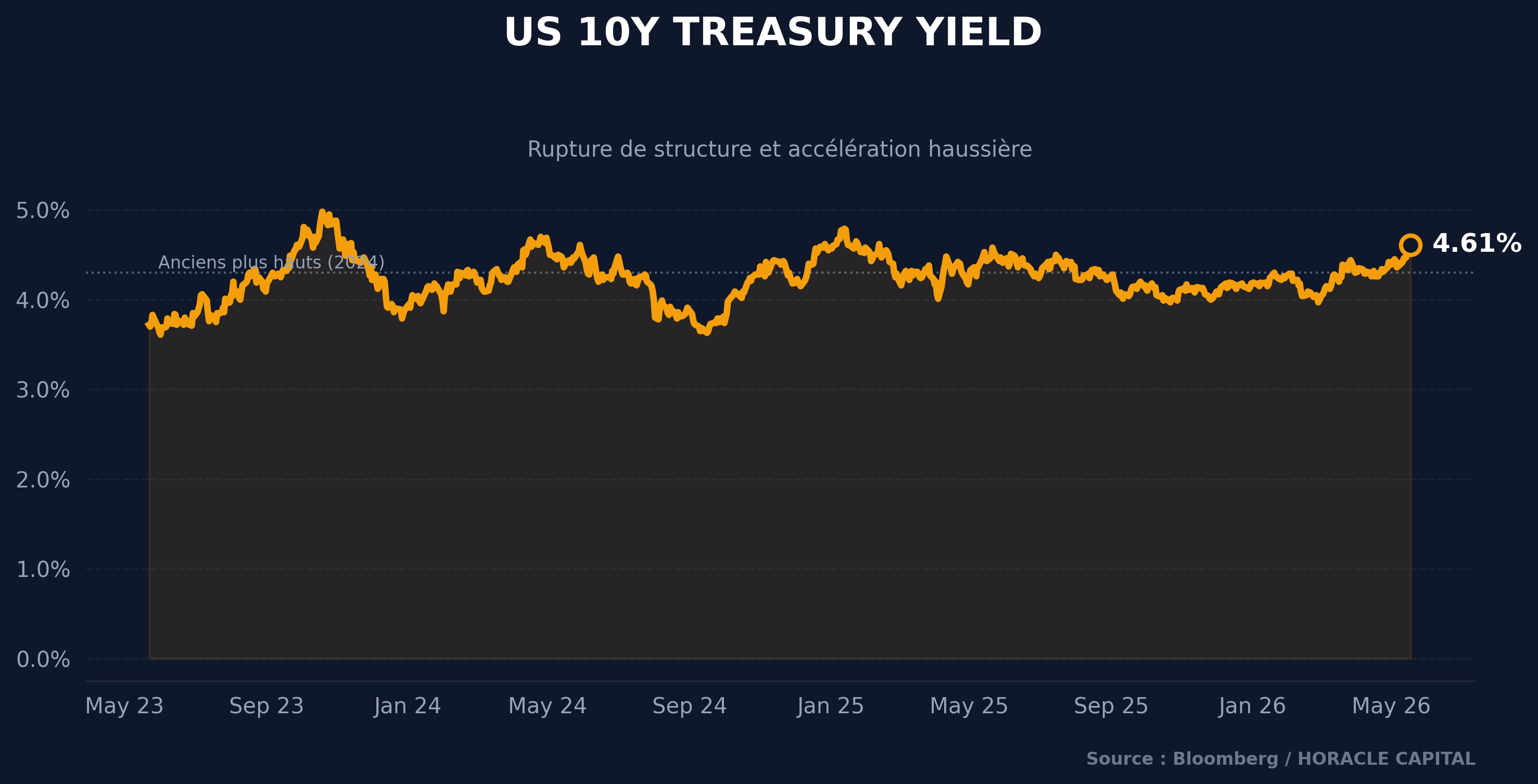

Long-term Treasury yields, notably the 10-year rate, have risen sharply. Faced with inflation risks fueled by rising energy costs, investors demand higher yield premiums and have thus reduced their exposure to long-duration bonds to limit their losses. This massive selling movement explains the surge in US rates, as bond prices move inversely to their yield.

Explaining the mechanism

The price of an existing bond varies inversely to market interest rates (yield). When an investor buys a bond, it pays a fixed interest called the coupon. If market rates rise, newly issued bonds offer a higher coupon, which makes the older bond less attractive and causes its market price to fall in order to align its yield with current conditions.

The consequences: why worry?

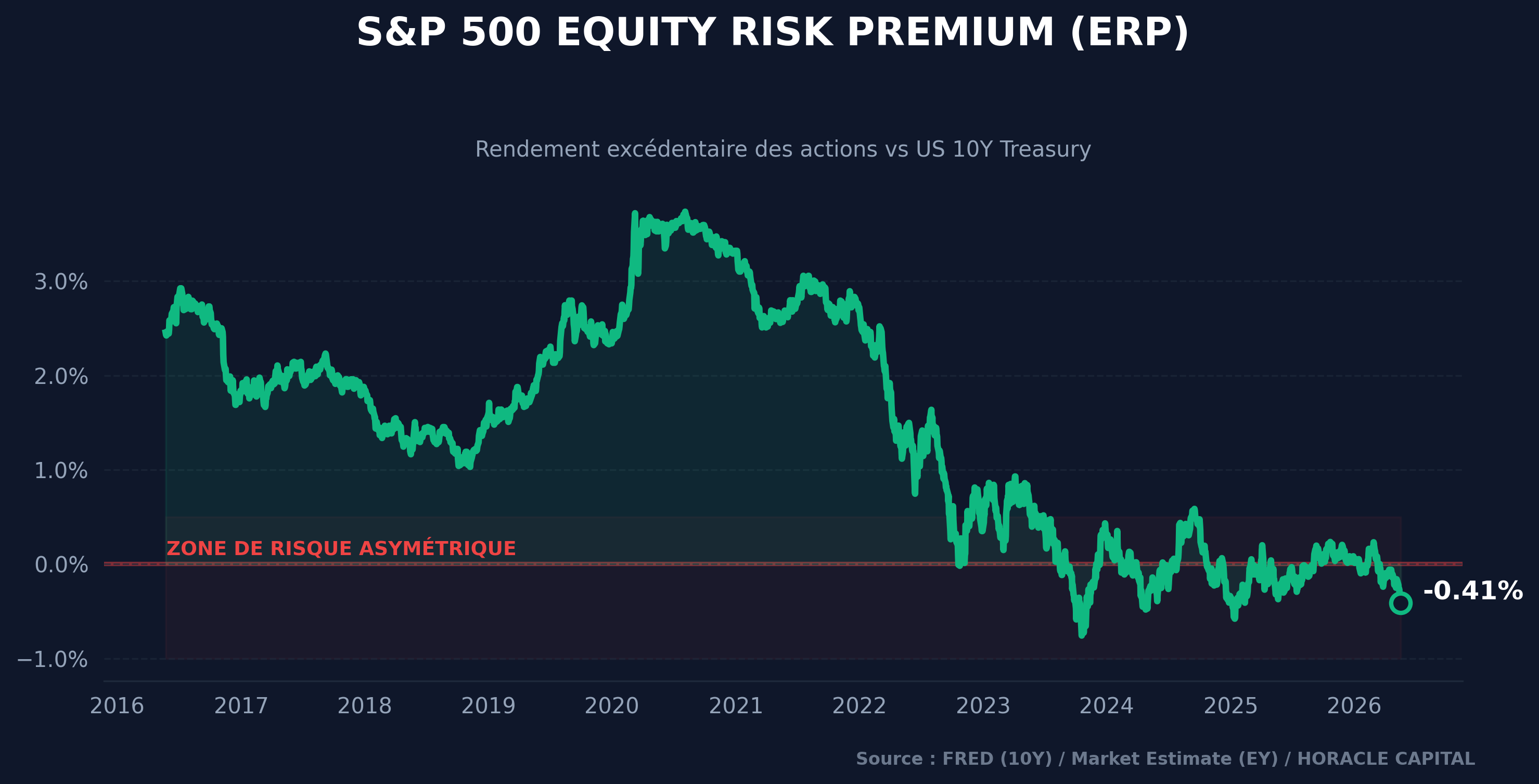

The compression of the Equity Risk Premium (ERP)

One of the most alarming signals of rising long-term yields is the compression of the Equity Risk Premium. The ERP represents the excess return investors demand for holding equities relative to risk-free government bonds.

Currently, the ERP is close to zero. This means the equity market offers almost no risk premium relative to Treasuries. In such a scenario, the trade-off becomes unfavorable to equities: why take the risk of equity volatility for a return you can obtain with Uncle Sam’s guarantee? It is a powerful driver for a correction or, at minimum, a stagnation of broad indices.

Impact on the real economy

This brutal rise in long-term yields has the consequence of a potential decrease in GNP, investment, and growth in general — here is why:

Investments, whether contracted by a household or a company, are relatively sensitive to the various rates, especially long-term rates given the rising average duration of loans. In the case of a company, an increase in the cost of credit would mean an ex post decrease in a project’s return, or else the abandonment of that project insofar as its return is below the risk-free rate (denoted rf). This contraction of investment also affects households, and thus obviously credit-driven sectors such as real estate, or large purchases (appliances, automobiles).

Over the long run, this aspect would result in a contraction of output and therefore, by extension, of workers’ income. As a result, a decline in wages leads to a decline in purchasing power and thus a contraction of domestic demand. Recession risks are then greater in the case of high long-term rates, because the structural dimension comes into play.

Valuation and the Financial Accelerator

Sovereign 10- and 30-year rates represent the world’s reference risk-free rate. According to the Gordon-Shapiro formula, a change in these rates directly modifies the discount rate applied to future cash flows, impacting the valuation of stocks and bonds. (The theoretical dimension is predominant in this argument.)

Moreover, high long-term rates increase the debt burden and compress the market value of assets pledged as collateral. This activates the financial accelerator, meaning that banks contract their supply of credit, which weighs on real economic activity — as with the case of companies and their investment seen in the first section.

Thus, to conclude, a rise in the domestic long-term interest rate relative to the foreign rate attracts international capital flows. The currency appreciates instantly in real terms, which deteriorates net exports and slows domestic output.

It is clear that the rise in long-term yields is not trivial; the impact remains real on the economy and on investments of all kinds.

How to take advantage of it?

(This is not investment advice)

So, in such a context, how can one take advantage?

First, the carry trade would be appropriate: already covered in several of our weekly reports, carry trading consists of borrowing in a low-rate currency (e.g. Japan), converting the loan into dollars, and buying US bonds. The yield differential, assuming an accommodating exchange rate, allows a gain for the borrower.

By virtue of the negative correlation between a bond’s price and its yield, a rise in long-term rates drives down the price of existing bonds. A controlled increase in your exposure to US T-bonds could be a very lucrative source of risk-free return.

Ultimately, the rise in the risk-free rate increases the discount rate in the discounted cash flow method. Growth stocks (the tech sector), whose cash flows are distant in time (long-term investment), see their fundamental value collapse. This opens up opportunities for short selling or strategic underweighting of these sectors in favor of short-horizon assets or cyclical sectors.

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →