Analysis of persistent inflationary tensions against the resilience of equity markets. A study of monetary divergences between the Fed, the ECB, and the dynamics in Japan, coupled with the awakening of commodities.

US

Inflation as the bête noire:

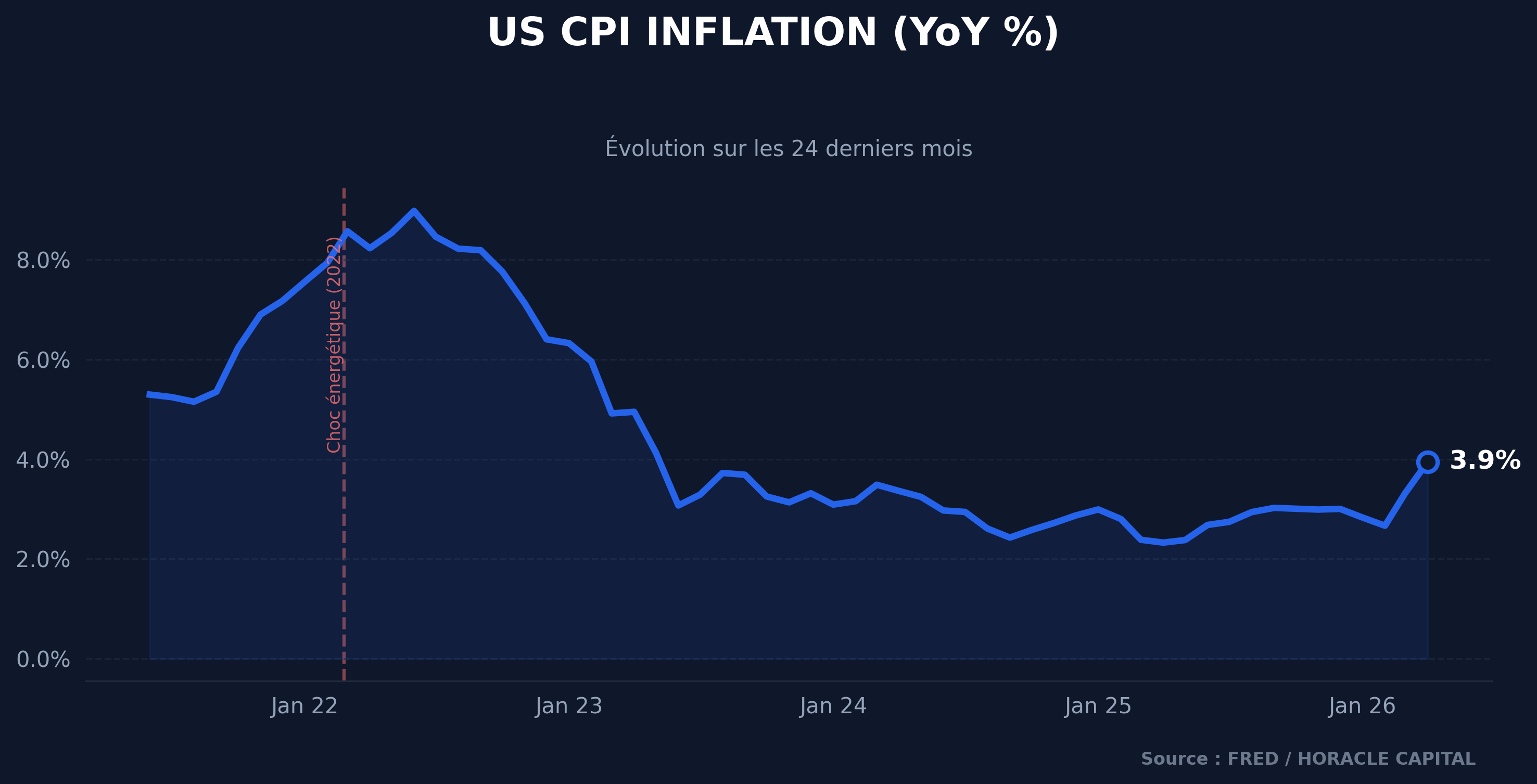

As we already highlighted in a previous report, Kevin Warsh is now the new chairman of the US Federal Reserve (Fed). Nevertheless, Jerome Powell still retains an important role within the Fed as he remains in the group of Fed governors. For now, a sense of uncertainty weighs on the various Fed rate expectations, with two fairly polarized stances that will have to work together to counter inflation. Because yes, the CPI data were quite shocking for most, with values (a rebound to 3.9% year-on-year) clearly above consensus expectations. As a reminder, the Fed’s mandate is dual (unlike the ECB, for example). Indeed, the Federal Reserve must monitor inflation with a 2% target but also unemployment to prevent it from spiraling too much.

This dual role forces decision-makers to make concessions at times, and with a relatively resilient labor market, this month’s inflation is likely to weigh on the Fed’s next decision. Obviously, this inflation does not come from nowhere; as we know, the war in the Middle East triggered a significant escalation in energy prices and thus in the production costs of most companies. With a growing AI sector, energy needs are colossal, and even though the US is considered energy-autonomous, it is no less impacted.

EUR

Just like the United States, the European zone is subject to significant inflation in the manufacturing and energy sectors. But here, given the European Union’s energy dependence, the impacts are likely to be greater, if not less controlled, than for the US, which is more sovereign from this standpoint. Thus, this has changed the rate-change expectations for the next meeting.

In terms of raw data, we saw a slight increase in growth in Germany and Italy. However, France is experiencing a period of stagnation with a strong penalty on the manufacturing sectors. The European outsider here will be Ireland, with a negative shock at the level of overall output.

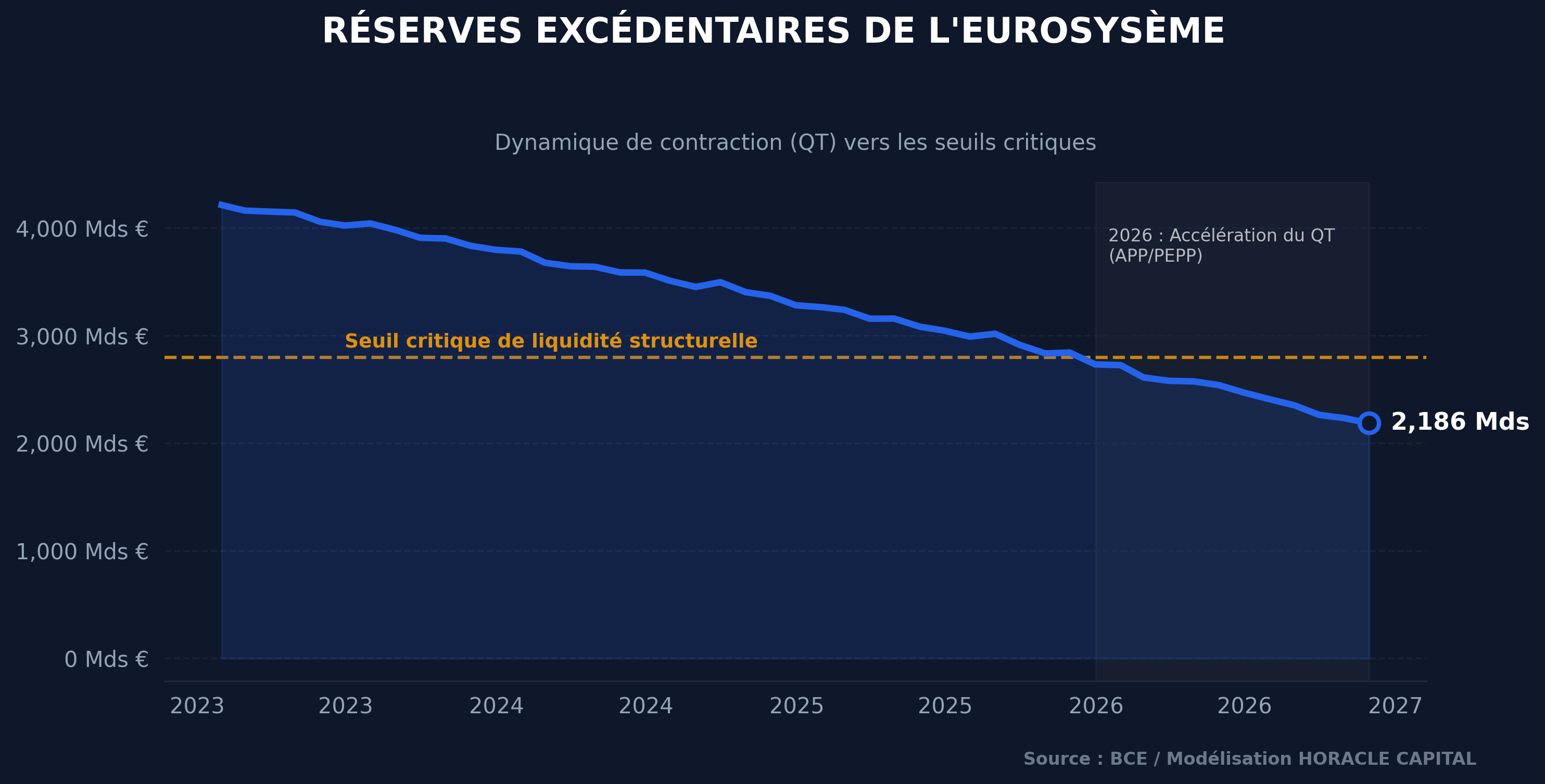

For the year 2026, the injection of paper on the secondary market will accelerate to exceed 500 billion euros, including 330 billion for the APP and 173 billion for the PEPP, even as commercial banks’ excess reserves burn down toward the critical threshold of their structural liquidity needs. On the financial front, this interest mismatch under the effect of past rate hikes results in a net loss of 1.3 billion euros for the ECB in 2025 versus 7.9 billion euros in 2024, a negative dynamic that is fading but that pushes the institution to plan a new long-term operational framework characterized by a permanent “structural bond portfolio” of reduced size and new long-term refinancing operations (LTRO).

Def:

- APP (Asset Purchase Programme): The ECB’s historic asset-purchase programme launched in 2014 to support the European economy and combat deflation.

- PEPP (Pandemic Emergency Purchase Programme): An emergency purchase programme implemented in the face of the pandemic to lower borrowing costs and stabilize the euro area.

- LTRO (Long-Term Refinancing Operations): Long-term refinancing operations allowing the ECB to provide abundant liquidity to European commercial banks.

Unlike the Fed, the ECB has only one main objective in its mandate: the 2% inflation target. However, employment remains a key and closely watched indicator, on the one hand by investors but also by the central bank’s analysts, in order to have an overall view of the situation in the relevant monetary zone. Unemployment data nonetheless rose in April to reach 7.5% in France and 3.3% in Germany. These two countries, being the main actors of the euro area and the most closely watched by the ECB, have a strong influence on decisions. Eurostat’s forecasts for the second half of the year suggest a marginally higher GDP, without much conviction.

Japan

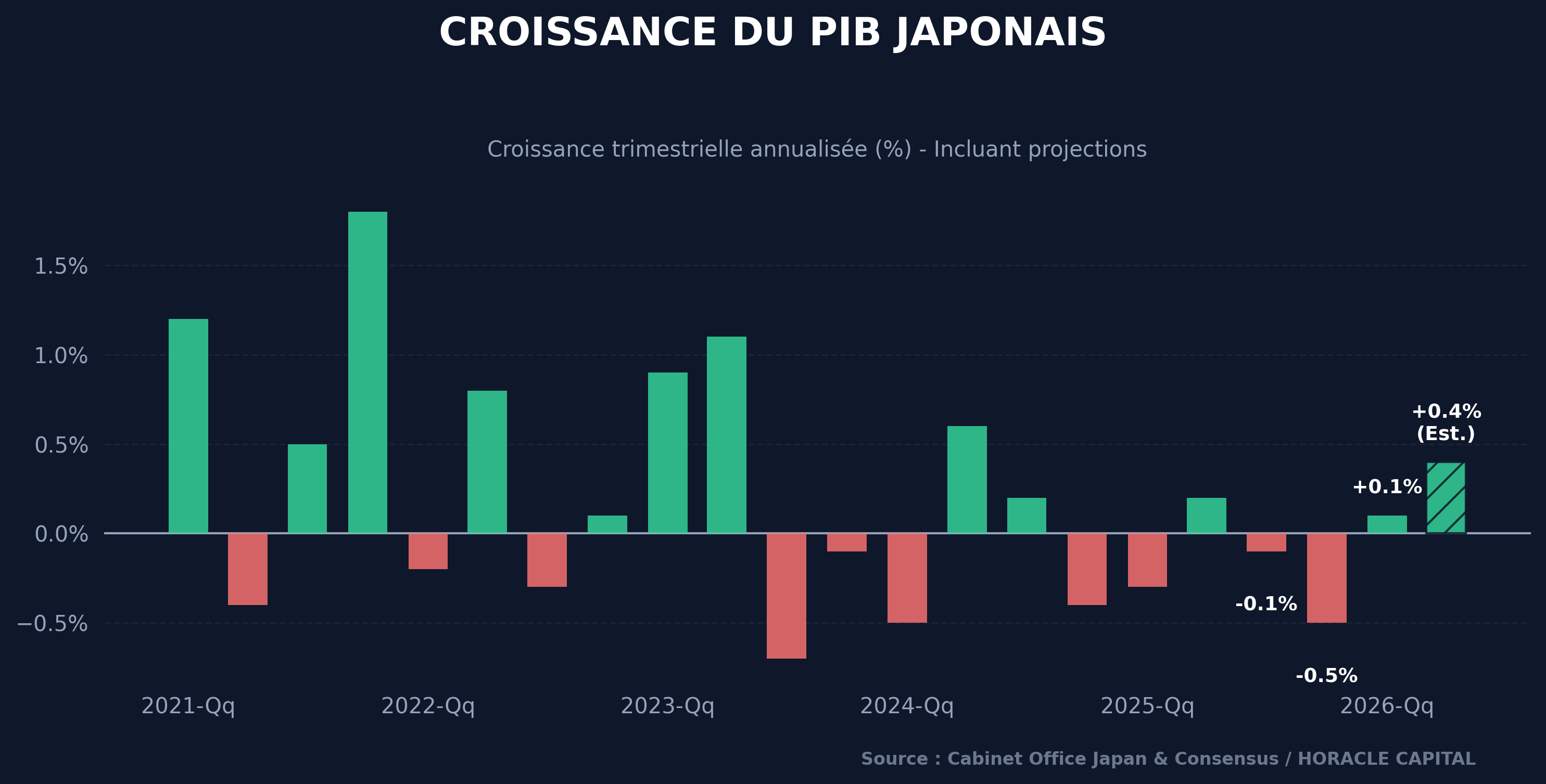

Japan could record its 2nd consecutive quarter of positive growth according to many research institutes. This Japanese-style resilience could herald higher inflation in the coming months. This dynamic is, in addition, supported by a rise in exports to the US and a surplus of public investment in productive areas.

Equities

On the equity front, the last two weeks have confirmed a paradoxical but tenacious dynamic. Despite the alarm signals on inflation and the revision of rate expectations by the Warsh-Powell duo, US indices continue to show insolent resilience. The S&P 500 and the Nasdaq absorb bad macroeconomic news as mere background noise, largely carried by technology stocks. AI remains the absolute safety net for institutional investors: the ability of these behemoths to generate free cash flow, even in an environment where the cost of capital looks set to be “higher for longer,” reassures markets. However, one must remain very cautious. The divergence between a tense macro (rising long-term rates, exogenous shocks) and indices at all-time highs creates a dangerous market asymmetry. The elastic is stretched to the extreme; at the slightest real crack in the US labor market, the backlash could be severe.

Commodities

On the commodities side, it is time for awareness. The recent renewed tension in the Middle East and the persistent diplomatic frictions have brutally reawakened the energy market. Crude experienced an aggressive rally over the last fourteen days, reintegrating a significant geopolitical risk premium into its prices. This oil shock is not trivial, because it is precisely what directly sabotages the disinflation efforts of Western central banks. But energy is not the only one to shine: industrial metals, copper in the lead, have also been highly sought after. This movement is explained by the combination of two factors: on the one hand, better-than-expected production data in the US and China, and on the other, the massive energy needs imposed by the global transition and the AI infrastructure boom. Commodities thus resume their historic dual role: a hedge against inflation and a direct barometer of global manufacturing activity.

Sources & References of the analysis

- ING

- Bureau of Labor Statistics (BLS)

- Federal Reserve Board (Fed)

- European Central Bank (ECB)

- Eurostat

- Bank of England (BoE)

- S&P Global Ratings

- Financial Times

- The Guardian

- Livemint

- Hindustan Times

- The White House

- Equals Money

- TradingView / ForexLive

- MaceNews

- BigGo Finance

- Tembo Money

- IndexBox

- The Mortgage Reports

- CBS News

- Institute for Government

- Electoral Commission

- Cambridge City Council

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →