The return of inflationary pressures via energy confines central banks within a narrow corridor.

The military conflict in Iran and the paralysis of the Strait of Hormuz have plunged markets into a phase of critical uncertainty. Roughly 20 million barrels per day are currently blocked, creating a supply shock that strategic reserves struggle to offset. This report analyzes the impact of this 100 $ oil on monetary policies and the relative resilience of the various economic zones.

The momentum is dominated by a growing divergence: while imported inflation pushes European central banks toward a hawkish stance, the deterioration of the US labor market is starting to temper the Fed's ardor, despite a dollar that remains the absolute safe haven.

1. USD: The postponement of rate cuts to 2027

Core PCE inflation, expected at 3.1%, forces the Federal Reserve to maintain a restrictive stance. Markets, which initially anticipated several cuts this year, now price only a single move, or even a complete postponement of rate cuts to 2027.

Yet the “employment paradox” becomes glaring: the latest NFP report showed a loss of 92,000 jobs with an unemployment rate climbing to 4.4%. The Fed finds itself caught between defending its inflation credibility (gasoline at 4.25 $/gallon) and an accelerating economic slowdown.

2. Energy: Oil as a weapon of mass demand destruction

Despite the IEA’s historic announcement releasing 400 million barrels of reserves, Brent remains glued above the 100 $ mark. The market seems skeptical about a swift resolution of the conflict, now pricing in a risk of several months of disruption in the Gulf.

US energy independence acts as a shield, explaining why the S&P 500 only retreats by 3% when European and Asian markets fall 6 to 9%. However, the cost of inputs (fertilizers, plastics, logistics) raises fears of durable recessionary inflation if the Hormuz blockage persists.

3. Analysis by Monetary Zone: The Divergence of Policies

Euro Area (EUR): The ECB faces the ghost of 2022. The market now prices a rate hike by July to counter energy inflation, even though the European economy is the most exposed to the shock. The 10-year swap rate heads toward 3%, a sign of extreme strain on long-term rates.

United Kingdom (GBP): The BoE is in a similar position, with inflation already above target. The market brutally dismissed hopes of a rate cut for 2026, pushing 2-year swap rates up by 50 basis points since the start of the conflict.

Australia & Canada (AUD/CAD): These are the big winners of the G10. Net energy-exporter status supports their currencies. The RBA is expected with a 70% probability of a rate hike on March 17.

Emerging Markets (EM): The shock is violent for energy-importing countries. The Hungarian Forint (HUF), the Chilean Peso (CLP), and the South African Rand (ZAR) suffer losses of 2.5 to 4% against the dollar owing to the explosion of their energy deficits.

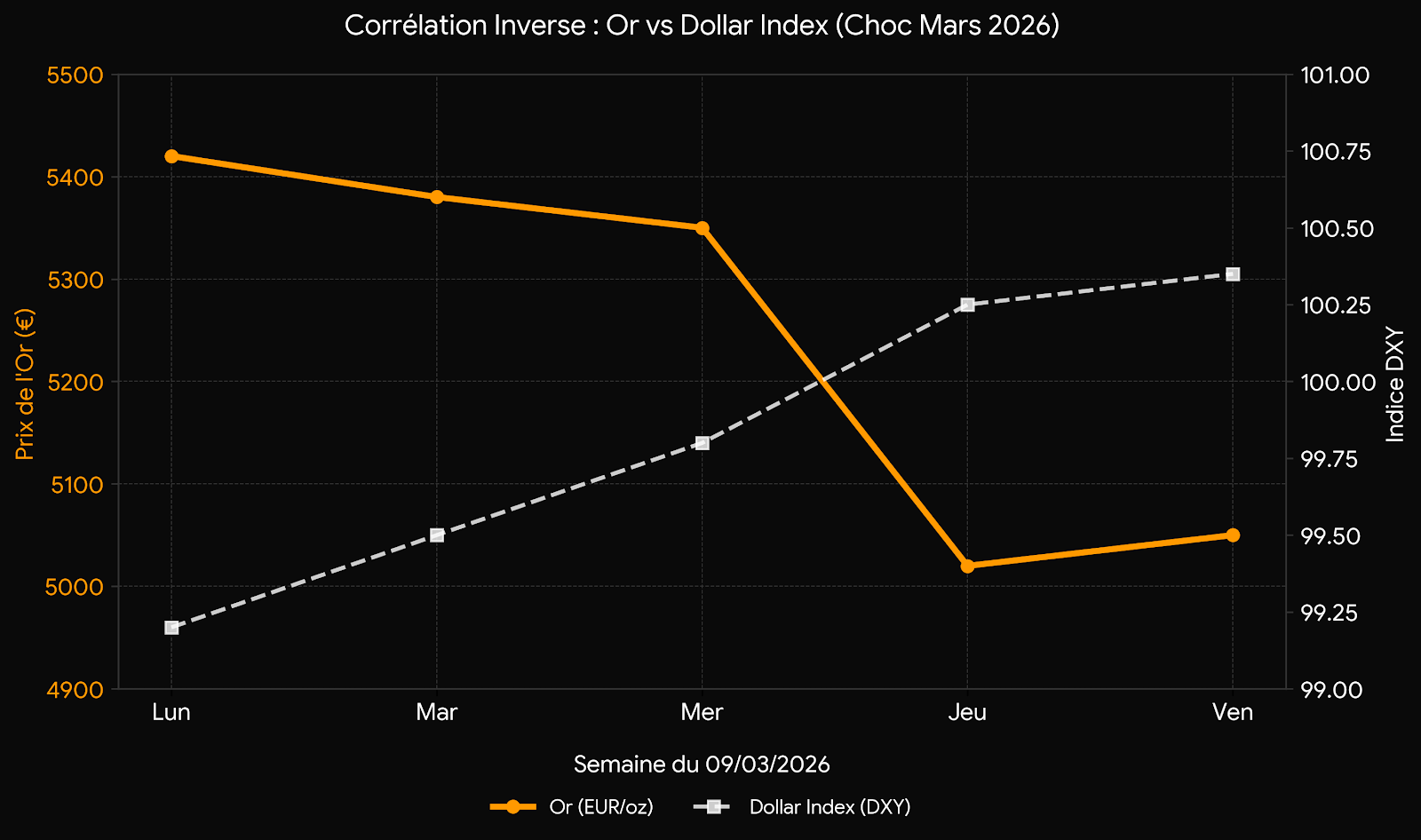

4. The Gold Enigma: Why is it falling in the middle of a war?

Last week, gold experienced a brutal correction, falling from 5,420 € to about 5,020 € an ounce, a loss of 400 € in one morning. For many retail investors, this move seems counterintuitive in a time of conflict.

The explanation lies in the massive strengthening of the Dollar: while oil remains expensive and maritime flows are paralyzed, the dollar imposes itself as the liquidity asset par excellence. Supported by an energy-autonomous US economy, the greenback, whose DXY index targets the 100.25/35 zone, mechanically raises the cost of gold for investors.

Moreover, the postponement of the Fed’s rate cuts to 2027 increases the opportunity cost of gold. In a period of forced deleveraging, capital abandons precious metals to take refuge in the remunerated safety of “King Dollar.”

| Asset | Level / Trend | Observation |

|---|---|---|

| Brent Crude | > 100 $ / barrel | Inability to replace the 20mb/d blocked despite the IEA. |

| USD (DXY) | Rising (100.25) | Absolute liquidity asset in the face of the energy shock. |

Trade Ideas & Opportunities

Long Dollar: As long as oil does not durably recede, the dollar will remain "bid" by default.

CAD & AUD: Take advantage of net energy-exporter status. The AUD remains supported by bets on an RBA hike (70% probability).

US Energy Names: Domestic producers are the big winners of high barrel prices without exposure to Gulf risks.

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →