The Davos forum and the return of volatility coincide with a resurgence of pressure on Japanese rates.

This week was peppered with economic data and announcements of all kinds, leaving little rest to most investors. At the start of the week, we observed a significant drop in equities, which eventually stabilized on Tuesday. This movement was accompanied by a lightning depreciation of the dollar and reassuring macroeconomic data for most monetary zones.

The volatility index VIX, a true "fear barometer," reached 20 points on Tuesday for the first time since November. Moreover, tensions related to Greenland seem to have stabilized, although caution remains in order: a simple announcement from Donald Trump Jr. could once again tip the market trend.

1. Trump & Davos: The “Taco Trade” and European relief

A major reversal marked the Davos forum this week. After threatening aggressive tariffs of up to 200% for certain sectors in France, in order to force the issue on the Greenland file, Donald Trump ultimately tempered his remarks following his meeting with Mark Rutte (NATO).

This strategic change of course removed the immediate threat of prohibitive tariffs. This “relief” allowed a significant rebound of European and US stock markets at the end of the week, a movement nicknamed “Taco Thursday” by some analysts.

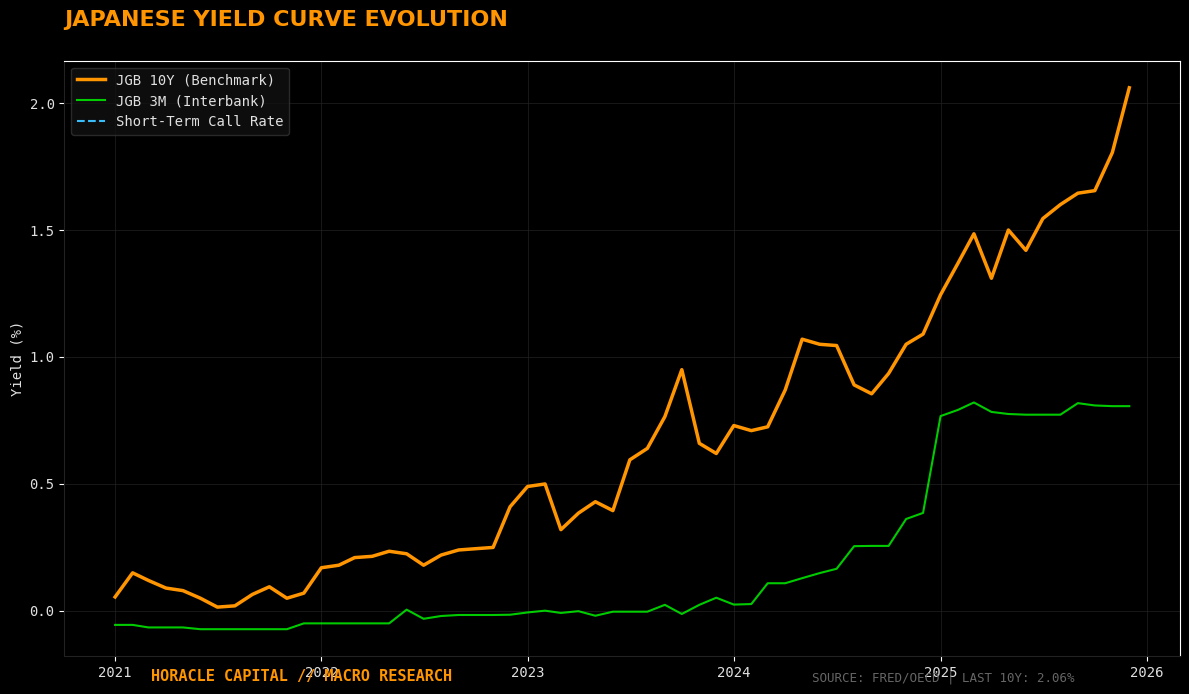

2. Bond Market: The critical alert on Japanese Yields (JGB)

An aspect often little covered, yet crucial, is the significant rise in Japanese yields. Bond rates in Japan have surged since the start of 2026, with a 10-year rate now exceeding 2.3%.

The macroeconomic stake is immense: if these rates remain high, Japanese investors’ interest in their own domestic bonds will increase drastically. This would push them to repatriate their capital, thereby abandoning US bonds (Treasuries) of which they hold nearly 17%. Direct consequence: to remain attractive, the United States would see its own yields rise, increasing the cost of overall debt.

3. Analysis by Monetary Zone: Deflation, Growth, and the ECB

Canada (CAD): The country faces a form of deflation with negative CPI data. The slowdown in prices in North America is marked, caused by US tariff pressures but also by the shock in Venezuela.

Australia (AUD): We observe an acceleration of the labor market and a decrease in unemployment. The stake for the RBA is now to monitor the next inflation figures to decide whether or not to maintain its restrictive stance.

New Zealand (NZD): Inflation is not alarming, going from 0.5% to 0.6% in quarterly variation. This could prompt the RBNZ to adopt a more accommodative tone to stimulate prices in the medium term.

United Kingdom (GBP): Inflation rose slightly while remaining above 2%. This figure aligns with a rise in manufacturing indices. The pound could remain supported if the BoE delays its rate cuts.

Euro Area (EUR): The summary of the ECB's December 17 meeting underlines fragile consumption. The zone's salvation will come through deep structural reforms and massive investments in defense and AI.

4. Commodities: Historic records and FOMO

Precious metals saw their prices explode last week. This rally was carried by the uncertainty linked to Trump’s policy and a massive phenomenon of FOMO (Fear Of Missing Out) on the part of investors.

The industrial stake is real: such expensive metals drastically increase the manufacturing costs of electronic chips, reducing the margins of tech manufacturers.

| Asset | Level Reached | Observation |

|---|---|---|

| Gold | 4,990 $ | Absolute all-time record, ultimate safe haven against disorder. |

| Silver | 103 $ | Price explosion, beyond all known technical ceilings. |

| Oil (WTI) | ~60 $ | Maintains a stable range despite strong tensions in Venezuela. |

5. Equities and Market Sentiment: “Sell America”?

Despite an eventful start to the week, stock markets showed resilience. We note, however, a marked sell-off on technology-sector leaders such as Google and Nvidia.

A “Sell America” sentiment seems to be emerging: many analysts think investors could abandon US assets in favor of better economic and financial stability in other zones, notably in Asia.

Trade Ideas & Opportunities

EUR/USD: The pair ended the week around 1.18 (exceeding our target of 1.17). Extreme caution is in order for the open: the dollar's depreciation was so brutal that a technical retracement is highly probable.

JGB / USD/JPY: The rise in JGB rates is a systemic risk to watch. If the movement accelerates, it will be a strong signal of Japanese capital repatriation.

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →