Analysis of the rise in US long-term yields, persistent inflation, and the monetary stakes between the Fed, the ECB, Japan, and the United Kingdom.

USD:

This week was marked by a sharp surge in US long-term yields, with very significant stakes, notably the risks of selling on the equity market (see the focus on long-term yields). This rise echoes persistent inflation in the US zone, and therefore even more restrictive expectations of the Fed’s decisions.

Indeed, the FOMC was held this week, with three distinct camps within the Fed’s governors. The majority, being the restrictive side, pushes back any easing of monetary policy owing to the behavior of oil futures, which lead to anticipating persistent inflation for several more months.

The dollar reaches its highest levels since 2022. Moreover, unlike last year when the risk premium demanded was related to fiscal pressures, this time it is linked to inflation.

As we saw this week, the US economy is even more autonomous than the other countries impacted by tensions in energy production. Thus, capital will tend to take refuge in the dollar to “play it safe,” all the more so as geopolitical tensions allow the dollar to retain its role as a refuge currency / store of value.

Euro:

This week, macroeconomic data did not live up to expectations, with fairly weak PMIs, attesting to a cyclical slowdown in euro-area activity. In fact, this decline in productivity seems to suggest that the ECB might not be as hawkish as the market had predicted.

The marked widening of the two-year swap spread in favor of the dollar illustrates the ECB’s inability to keep pace with the Fed’s restrictive tempo. The European institution faces a markedly more degraded growth/inflation trade-off, which removes the rate cushion that protected the single currency during previous crises.

ECB Rate Expectations - June 2026 Meeting:

| Priced Move (Source: Polymarket) | Probability |

|---|---|

| +25 bps Hike | 87% |

| Status Quo | 13% |

| +50 bps or more Hike | 1% |

| -25 bps Cut | <1% |

| -50 bps or more Cut | <1% |

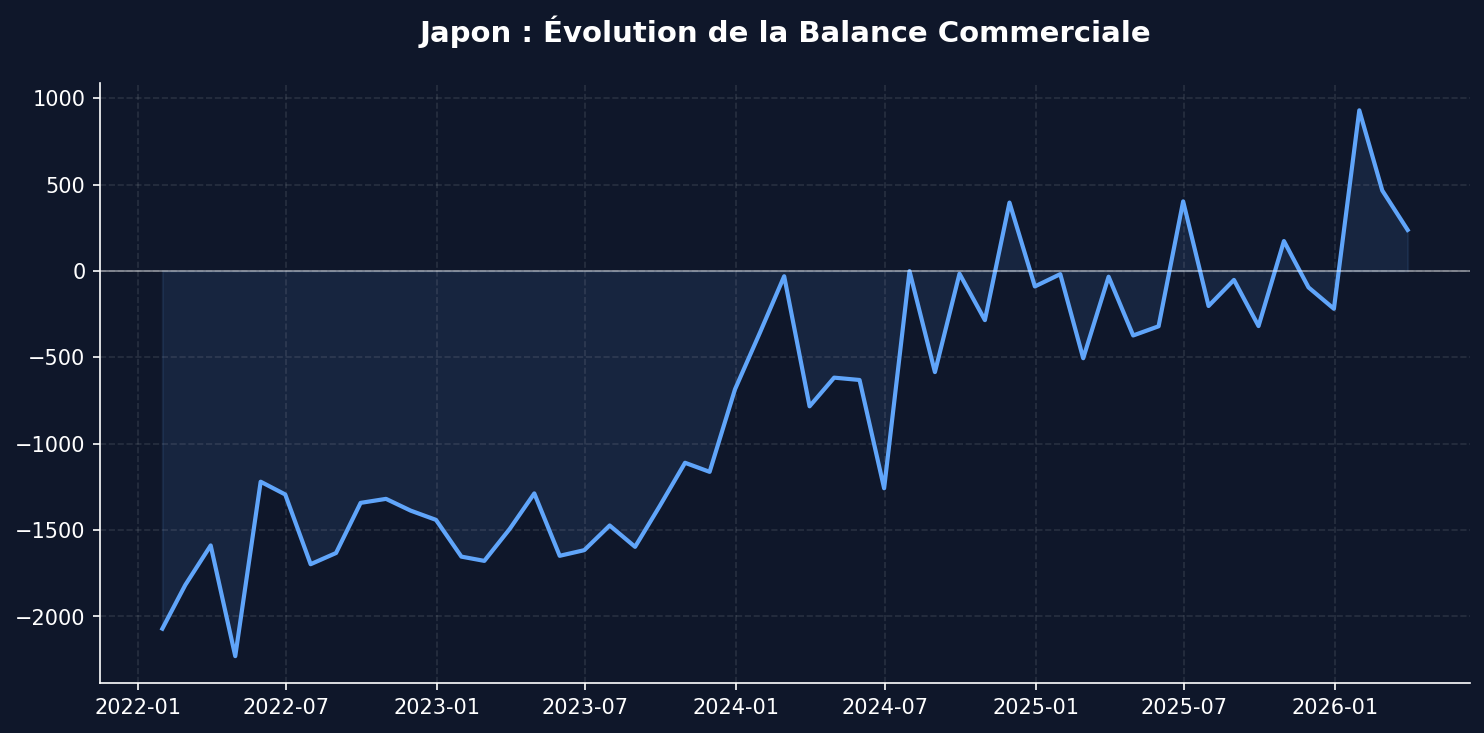

JPY:

Against all expectations, Japan published a positive figure, that of the trade balance. On the FX market, a positive trade balance generates a structural JPY-buying flow via the repatriation of invoicing revenues from large Japanese exporters. This net trade flow softens speculative selling pressure and offers an endogenous alternative to the Ministry of Finance’s sterilized direct interventions on FX reserves, after the massive drawdowns estimated at nearly 70 billion USD in April/May. Because indeed, we saw a deployment of large volumes of FX reserves by the Japanese authorities to defend their currency. Even though expectations of Japanese rate hikes are already digested by the market, the structural depreciation dynamic itself persists.

GBP:

Political tensions and the marked slowdown in domestic inflation invalidate the scenario of aggressive monetary tightening initially priced by the market, which had been counting on several consecutive rate hikes from the BoE. The release of April’s consumer price index (CPI) at 2.8% YoY, combined with a slight slowdown in activity and unemployment above expectations, confirms that the monetary tightening planned by the central bank no longer seems to be a necessity, but rather an option, with the probability for the June meeting now calibrated at 50:50. With inflation expected to peak just below 4% later this year, investors are forced to reassess the interest-rate trajectory in light of these macroeconomic data.

This deterioration of the fundamentals weakens the pound sterling at the very moment when the British political situation remains fluid and uncertain, threatening to steer economic policy to the left. Although the GBP finds partial technical support in the appeal of the carry trade thanks to a high 3.75% yield amid declining FX volatility, the combination of weakened growth, heavy political risks, and a poorly priced BoE cycle clearly accentuates the currency’s structural vulnerability for the summer period.

Sources & References of the analysis

- Federal Reserve Board (Fed)

- European Central Bank (ECB)

- Bank of England (BoE)

- ING Think

- The Financial Times

- FRED API (Federal Reserve Economic Data)

- Polymarket (Rate pricings)

- S&P Global PMIs

- NVIDIA Investor Relations

Ready for the next step?

Don't miss any signal. Join our research community for unrivaled macro analysis and quantitative models.

Léo Lombardini

Trader, Economics & Quant

Passionate about market analysis and statistical modeling, Léo oversees the strategic allocation of the model portfolio and the development of Horacle Capital's quantitative frameworks, as well as writing weekly articles.

Learn more about the author →